by Eric Worrall

“… SVB recognizes the significant societal, ecological and economic threats of climate change. … We enable entrepreneurs with inventions and new businesses that reduce greenhouse gas (GHG) emissions and take seriously the responsibility to reduce our own. …” – SVB ESG Report 2022 Section 8

Pinkerton: Green, Woke, and Now Broke — How SVB Became the 2nd Biggest Bank Failure in U.S. History

Go Woke, Go Bust

Oh so woke, oh so green, oh so diverse Silicon Valley Bank (SVB) just went bust.

One can go to its website—still up for who knows how much longer—and see that it claimsassets of $212 billion. But as they say, the bigger they are, the harder they fall; and so SVB makes for the second largest bank failure in U.S. history.

…

Speaking of ‘splaining, SVB officials will need to answer a lot of questions, including, What role did wokeness play in SVB’s failure?

Another term for wokeness, of course, is ESG, which stands for environmental, social, and governance. ESG is a pertinent question, as there’s a considerable body of economic literature showing that woke investments aren’t good investments. For instance, one study by professors at the London School of Economics and Columbia University finds that:

ESG funds appear to underperform financially relative to other funds within the same asset manager and year, and to charge higher fees. Our findings suggest that socially responsible funds do not appear to follow through on proclamations of concerns for stakeholders.

…

Of course, it wasn’t just the woke policies of SVB which might have contributed to the disaster. One of the biggest sources of damage to Silicon Valley Bank was the bank’s mistaken belief that fixed rate securities were a safe harbour for depositor’s money.

From Forbes;

How Jerome Powell Killed Silicon Valley Bank

…

With a hat tip to this fine Mint.com explainer, the oversimplified sequence of events is:

- Silicon Valley Bank’s deposits grew from $61 billion at the end of 2019 to $181 billion at the end of 2021, as its startup customers raised ample VC money.

- This was too much of a good thing; Silicon Valley Bank couldn’t lend these deposits out quickly enough, so it began looking for something else to do with this money.

- Unfortunately, a large part of that “something else” happened to be very long-dated (i.e., maturities in excess of 10 years) mortgage-backed securities (MBSes). Silicon Valley Bank put 56% of its assets into fixed-rate securities, which is far higher than most banks.

- Whether it was fully or semi-deliberate, Silicon Valley Bank was betting heavily on interest rates not rising.

- As interest rates rose – one-year Treasuries, for instance, went from yielding around 0.05% (on May 31, 2021) to more than 5% these days – the values of those MBSes cratered.

- Moody’s downgraded Silicon Valley Bank.

- People worried about Silicon Valley Bank. Peter Thiel and other VCs advised portfolio companies to withdraw their money. Account holders had already been withdrawing deposits in 2022 as funding slowed, so convincing them to withdraw more wasn’t hard.

- To provide this money, Silicon Valley Bank had to sell already-depressed assets at fire-sale prices.

- (Silicon Valley Bank also told people “we’re OK” when they were very much not OK, which likely worsened the panic.)

- Silicon Valley Bank, with $209 billion in assets, became the second-biggest US bank failure ever. FDIC insurance covers $250,000 in deposits, but as Silicon Valley Bank is a business bank, less than 3% of its deposits are covered.

- Incidentally, with $620 billion in unrealized losses at other US banks, people are worried about a similar fate at other small, undiversified banks, and bank stocks are tanking overall.

Forbes is wrong to blame Jerome Powell. Rising interest rates are a symptom of economic crisis, not the cause.

One of the Federal Reserve’s main responsiblities is to ensure price stability, to contain inflation to around 2%. If inflation is allowed to soar unchecked, if interest rates are not increased to combat rising inflation, the result could be a deep recession, or even a second Great Depression. High inflation rates scramble market signals. Entrepreneurs pile their money into asset bubble sectors – houses, race horses, fine art, tulips, whatever happens to be fashionable, instead of focusing on real businesses and job creation.

So what caused the instabilities which forced the Fed to raise interest rates?

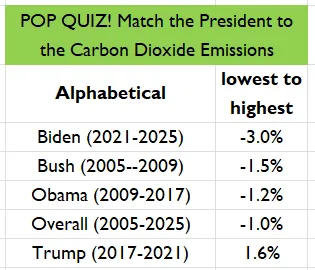

I would argue the Biden administration created the economic crisis which forced the Fed to raise interest rates, with their wild Net Zero spending spree, and their hostility towards fossil fuel.

Gasoline and energy inflation is a major component of the consumer inflation which the Fed is dedicated to managing. As WUWT has repeatedly documented, the Biden administration’s reckless spending on Net Zero, and hostility to domestic drilling, is largely responsible for the spike in energy prices and consumer inflation.

Could a different President have done better than Biden? The likely answer is yes. If President Trump’s America First energy policies had been continued, abundant domestic supply would have kept gasoline pump prices more under control, and cheap energy exports would have driven up the value of the US Dollar, which in turn would have counterbalanced the impact of global commodity price rises.

I’m not claiming there would have been zero inflationary pressure or interest rate hikes, but there would have been no hesitancy over releasing Federal land for drilling, so America would have been in a better position to laugh off supply shocks. And the US Secretary of State wouldn’t have had to go crawling to a wanted accused felon, apparently to secure US rights to pump Venezuelan oil.

The only remaining question, will the Republican Congress cave in to demands for a bank bailout? In my opinion there will be huge pressure on Congress this week to mount a bailout, to use YOUR money to rescue the rich liberal clients of Silicon Valley Bank, you know, the radical left wing silicon valley giants who helped Federal Government agencies suppress and censor conservatives and climate skeptics.

I can’t tell any of you what to do, but I urge you all to write to your Congress representatives, to let them know exactly how you feel about your hard earned potentially being used to bail out the Silicon Valley Bank wokesters, before your representatives get all their time booked by smart lobbyists in expensive suits flying in from California.

h/t SMC – looks like the Biden administration doesn’t need approval from Congress to release money to Silicon Valley Bank depositors :- https://finance.yahoo.com/news/us-government-guarantees-all-silicon-valley-bank-deposits-money-available-monday-223546372.html